Oil hits nearly 6-month highs as US says it will end Iran sanctions waivers

Oil prices spiked on Monday — past highs not seen since last fall — after reports that Washington is set to announce that all buyers of Iranian oil will have to end imports, or be subject to U.S. sanctions.

The White House confirmed the reports on Monday morning.

Brent crude futures surged more than 3% to $74.31 per barrel on Monday, sailing past last week's 2019 high at $72.27 and hitting the highest level since Nov. 1, 2018. Brent, the international benchmark for oil prices, was last up $1.82, or 2.5%, $73.79.

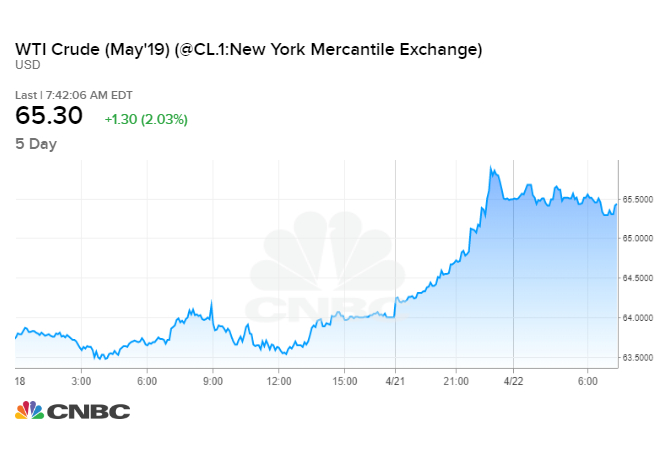

U.S. West Texas Intermediate crude futures rose $1.52, or 2.4%, to $65.52 per barrel, after hitting $65.87, its highest level since Oct. 31, 2018. WTI had been trading sideways after hitting a 2019 high at $64.79 nearly two weeks ago.

That price spike followed a report by the Washington Post, citing two unnamed State Department officials, that U.S. Secretary of State Mike Pompeo will announce that the State Department will cease granting sanctions waivers to any country still importing Iranian crude or condensate, an ultra-light form of crude oil, after May 2.

"The sanctions (are) obviously one of the major movers, I think, which is influencing prices," said Daryl Liew, head of portfolio management at financial services company Reyl Singapore. He also pointed to stronger-than-expected economic growth data from China last week, which could be driving demand expectations.

Brent prices have risen by more than a third this year following a collapse in the cost of crude in the final months of 2018. U.S. crude has soared 44 percent year to date.

The U.S. reimposed sanctions in November on exports of Iranian oil after U.S. President Donald Trump unilaterally pulled out of a nuclear accord struck in 2015 between Iran and world powers. Washington, however, granted eight of Iran's biggest oil buyers exemptions that allowed them limited purchases for an additional six months.

The eight buyers are China and India — Iran's biggest customers — as well as Japan, South Korea, Italy, Greece, Turkey and Taiwan.

Of the buyers of Iranian oil, Liew said India could suffer the most from Washington's move.

"I think India is probably one of the key potential countries that might suffer from a higher oil price, in terms of their current account deficit, for example. And that's going to be basically putting pressures on inflationary pressures as well," Liew said, speaking on CNBC's "Street Signs" on Monday.

"No doubt the Indian central bank has ... turned to a more dovish stance in recent meetings. But if oil prices continue to hit higher, and inflationary pressures come back into the picture again for India especially, then the central bank probably has to reverse the dovish moves," he concluded.

The waivers have allowed Iran to continue exporting about 1 million barrels per day, down from roughly 2.5 million bpd last year.

The development on sanctions comes as global oil supply is already tightening, with OPEC leading supply cuts since the beginning of this year, to prop up crude prices.

OPEC and its oil market allies, including Russia, have aimed to keep 1.2 million bpd off the market since January. The group next meets at the end of June to decide whether to lift the production caps or continue suppressing output.

In a statement, the White House said the U.S. will work with OPEC members Saudi Arabia and the United Arab Emirates "to take timely action to assure that global demand is met as all Iranian oil is removed from the market."

Meanwhile, major OPEC oil producer Libya's capital Tripoli was hit by a series of airstrikes and explosions over the weekend, in escalating violence that could threaten oil supply further.

The country has been torn by conflict since the fall of dictator Muammar Gaddafi in 2011. It was sent into fresh conflict in recent weeks after its eastern military leader ordered his forces to move in on the capital where the United Nations-recognized government sits.

Analysts and traders keep a close eye on Libya because its oil production has been one of the biggest wild cards in the oil market in recent years. Its output has fluctuated wildly as the nation's southern oil fields have frequently gone offline amid fighting.

One analyst told CNBC on Monday that the Libya situation will put more pressure on oil prices, particularly if the conflict escalates.

"Libya is producing 1.1 million barrels per day. If things go wrong, immediately somewhere around 300,000 to 400,000 barrels per day of oil may be affected," said Kang Wu, head of analytics for Asia at S&P Global Platts.

"A lot depends on how Saudi Arabia will react to the situation — they have surplus capacity — but supply concerns will keep pressure on oil prices in the short term," Wu added.

In the U.S., energy firms last week reduced the number of oil rigs operating by two, to 825, General Electric's Baker Hughes energy services firm said in its weekly report on Thursday.

— Reuters contributed to this report.

Read More

About Live World News

No comments